Really its all about you...

To set you on the right financial path, we must understand your unique situation. We do this through a Financial Needs Analysis.

The Rule of 72.

The Rule of 72 is a quick way to estimate the number of years required to double your invested funds at any given rate of return. It works by dividing the rate into 72. For example, money invested at a 3% rate of return, should double in 24 years. And money invested with a 7% rate should double in 10 years.

The Magic of Compounding.

When the interest on your investments earns interest, it allows you to save more in the long run. If you start with $1,000 with an interest rate of 4%, simple interest will provide you with an extra $40 at the end of the year. When you compound, you’ll continue to gain interest on your original investment, but also on the interest you already earned.

Don’t get stuck with a policy that doesn’t properly protect your family.

Term life policies are easier to understand and more affordable than whole life insurance. A 30-year-old male, for example, may pay around $4,675 a year for whole life versus only $242-$403 a year for term life.2

This cost difference allows you to invest the saved money and/or apply it toward a debt—bringing your financial wellness plan full circle

2 “The Differences Between Term and Whole Life Insurance” NerdWallet, March 29, 2017

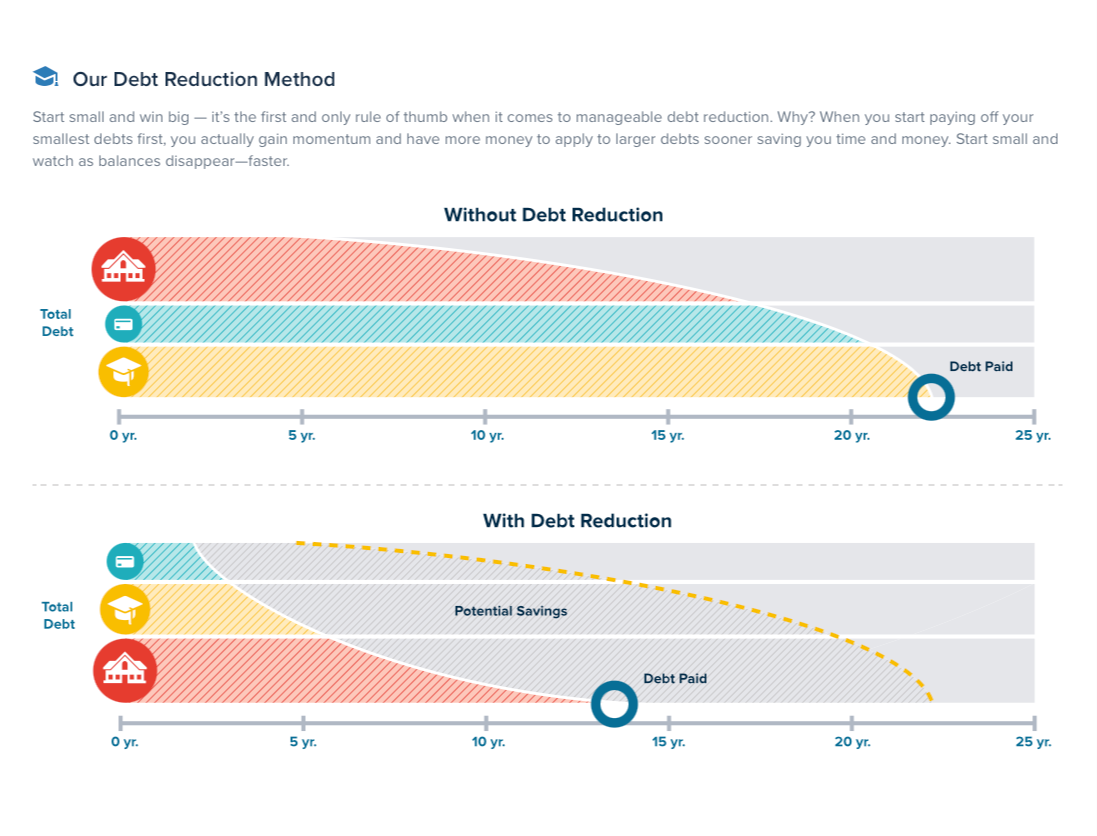

With an actionable debt reduction plan, you’ll be on your way to financial independence.

We get it. The debt reduction process is overwhelming. Determining the best plan, and sticking to it, takes discipline and budgeting. But it gets easier as you go, especially as your remaining balances reduce and, eventually, disappear.

The debt reduction method is a great place to start. Pay off debts, starting with the smallest, and watch as balances disappear. The more you pay off, the more available funds you have to put toward remaining debts. Like riding a bicycle downhill, your debt reduction plan gains momentum and becomes easier and less overwhelming over time.

Client Centered

Whether you are investing to build wealth, protect your family, or preserve your assets, our personalized service focuses your needs, wants, and long-term goals.

Our team of professionals have years of experience in financial services. We can help you address your needs of today and for many years to come. We look forward to working with you.